Donor Advised Funds: A Unique Way to Give (and Save on Taxes)

Donor-advised funds (DAFs) are a super unique tool when it comes to financial planning. They are extremely helpful if you want to be charitable and tax-smart. A DAF lets you donate now, get a tax deduction today, and decide later where the money goes. It’s a useful tool for high-income years, asset sales, or when your charitable giving strategy needs more flexibility.

What’s a Donor Advised Fund?

Think of a DAF as a charitable investment account. You contribute cash, stocks, or other assets into the fund. You get a tax deduction in the year you donate. The money grows tax-free inside the account. You recommend grants to charities over time.

You don’t have to decide today who gets the money—you can wait, invest the funds, and distribute later.

Key Tax and Planning Benefits

Deduct now, give later: You get the full deduction in the year you contribute. Up to 60% of AGI for cash, 30% for appreciated assets.

Avoid capital gains: If you donate appreciated stock or real estate, you skip capital gains taxes and deduct the full value.

Tax-free growth: Contributions can be invested in the DAF and grow without tax drag while you decide on giving.

One receipt: Instead of tracking gifts to 10 nonprofits, you get one receipt for your DAF contribution.

Legacy planning: You can name a successor advisor—kids, spouse, etc.—to continue your giving plan after you’re gone.

When DAFs Make Sense

High-income year – Business sale, bonus, RSU vesting? Front-load your giving now.

Charitable intent, no clear cause yet – Deduct this year, decide later.

Appreciated assets – Like stock bought long ago with low cost basis. Avoid the tax hit.

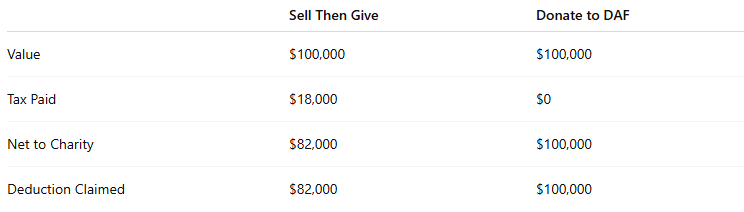

Example:

Let’s say you own $100,000 of stock purchased for $10,000. If you sell it, you’ll owe ~$18,000+ in capital gains tax. If you donate it to a DAF:

The DAF route gives the nonprofit more and boosts your deduction.

Strategic Moves We See Often

Bunching two or three years of giving into one DAF contribution to exceed the standard deduction.

Offloading pre-IPO stock, real estate, or business interests before a liquidity event.

Using a DAF in combination with a charitable remainder trust or gifting strategy.

Downsides to Know

No guaranteed timeline – There’s no rule that forces donors to distribute quickly.

No control – You “advise” on grants, but the fund technically owns the money.

Current Trends

Over $250 billion is now held in DAFs.

Average payout rates are high (around 20%+), even though no minimum exists.

New low-cost DAF platforms are targeting younger and mass-affluent donors.

There’s growing legislative interest in forcing minimum annual distributions.

Note that this can also change if new laws are passed. Refer to the chart below for historical levels.

Should You Use a DAF?

A DAF is a fit if:

You want to make a tax-deductible gift this year, but spread grants over time.

You’re donating appreciated assets and want to avoid the tax hit.

You prefer simplicity and one source to manage your giving.

Not a fit if:

You want complete control over the funds (consider a private foundation instead).

You plan to make only small, one-time donations and don’t itemize.

Bottom Line

Donor advised funds are simple to open, flexible to use, and powerful in the right context. If you’re facing a spike in income or want to build a structured charitable strategy without creating a private foundation, this tool can check both the tax and planning boxes.

Related Guides:

Our Process for Reviewing Your Tax Plan

Maximize Wealth Transfer: 2025 Gifting Rules and Tax-Saving Strategies