Is it a good idea to invest when the market is at an all-time high?

Markets keep making headlines for hitting all-time highs. If you’re retired or nearing retirement, that can feel unsettling. You may wonder if now is the wrong time to invest or if you should pull back. But history tells a different story. Markets reaching records is not rare—it’s normal. The challenge isn’t timing the market; it’s building a plan that works through highs and lows.

All-Time Highs Happen More Than You Think

The S&P 500 has hit thousands of all-time highs over the past century.

Markets spend most of their time within 5% of record levels.

New highs often lead to more highs, not sudden crashes.

Charts show this clearly: the long-term trend of the market is upward, with regular corrections along the way. Sitting out at new highs often means missing the strongest growth periods.

On average, 12-month returns following an all-time high being hit have been better than at other times: 10.4% compared with 8.8% when the market wasn’t at a high. Returns on a two- or three-year horizon have been similar, regardless of whether the market was at an all-time high or not.

12-Month Returns: Higher After All-Time Stock Highs Average Inflation-Adjusted Returns for US Large-Cap Equities

Why Retirees Worry

Retirees face different risks than younger investors. Your biggest concern isn’t maximizing growth; it’s protecting income and making your money last.

Sequence of returns risk: A major drop early in retirement can hurt long-term income.

Inflation risk: Holding too much cash means your money buys less over time.

Longevity risk: Retirement can last 25–30 years, so you need growth to support future income.

These risks can create fear when the market is at records, but they’re best managed with structure, not guesses about timing.

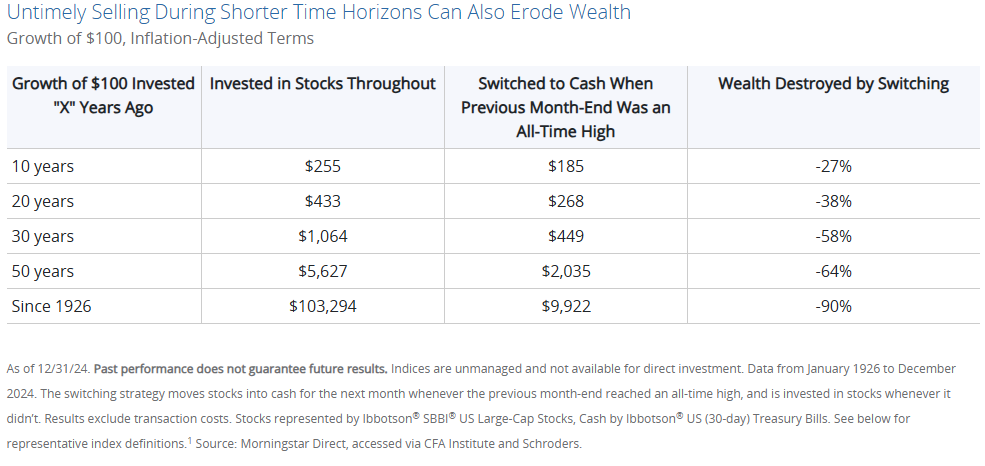

Even over shorter horizons, investors would have missed out on a lot of potential wealth if they’d been frightened away whenever the market was riding high.

A Smarter Approach Than Market Timing

Segment your assets by time horizon

Short-term (1–3 years): Hold cash or short bonds to cover living expenses.

Medium-term (3–10 years): Use income-producing investments like bonds, dividends, or real estate.

Long-term (10+ years): Keep growth-focused stocks that can ride out volatility.

Use an income bucket strategy

Withdraw from stable assets in down markets.

Let growth investments recover before tapping them.

Rebalance regularly

Sell from winners to refill your safe bucket.

Buy into areas that have pulled back.

Manage taxes as carefully as investments

Coordinate withdrawals across taxable, tax-deferred, and tax-free accounts.

Plan Roth conversions or charitable gifts in low-tax years.

Final Thoughts

All-time highs shouldn’t scare you out of the market. They’re a normal part of long-term investing, and history shows they often lead to more growth. What matters most in retirement isn’t predicting the next market move—it’s having a plan that balances income, protection, and growth.

If you’re unsure how your retirement portfolio would handle the next correction or the next high, it may be time to review your strategy. A disciplined income plan can give you confidence no matter where markets sit today.

Visit my site -> finnprice.com

Education on a Weekly Basis -> Newsletter

Subscribe to the Youtube Channel for more video content -> Finn Price Youtube

About the author: Finn Price, CPFA, CEPA, is a business owner and wealth manager at Railroad Investment Group. He helps successful entrepreneurs & individuals with concentrated stock positions in their 30s, 40s and 50s build, organize, protect and transfer their wealth.

Note: this article is general guidance and education, not advice. Consult your money person or your attorney for financial, tax, and legal advice specific to your situation.

Securities and advisory services offered through LPL Financial, a registered investment Advisor, Member FINRA/SIPC.