Tax-Efficient Investing: How to Mind the Tax Funnels and Harvest Gains & Losses

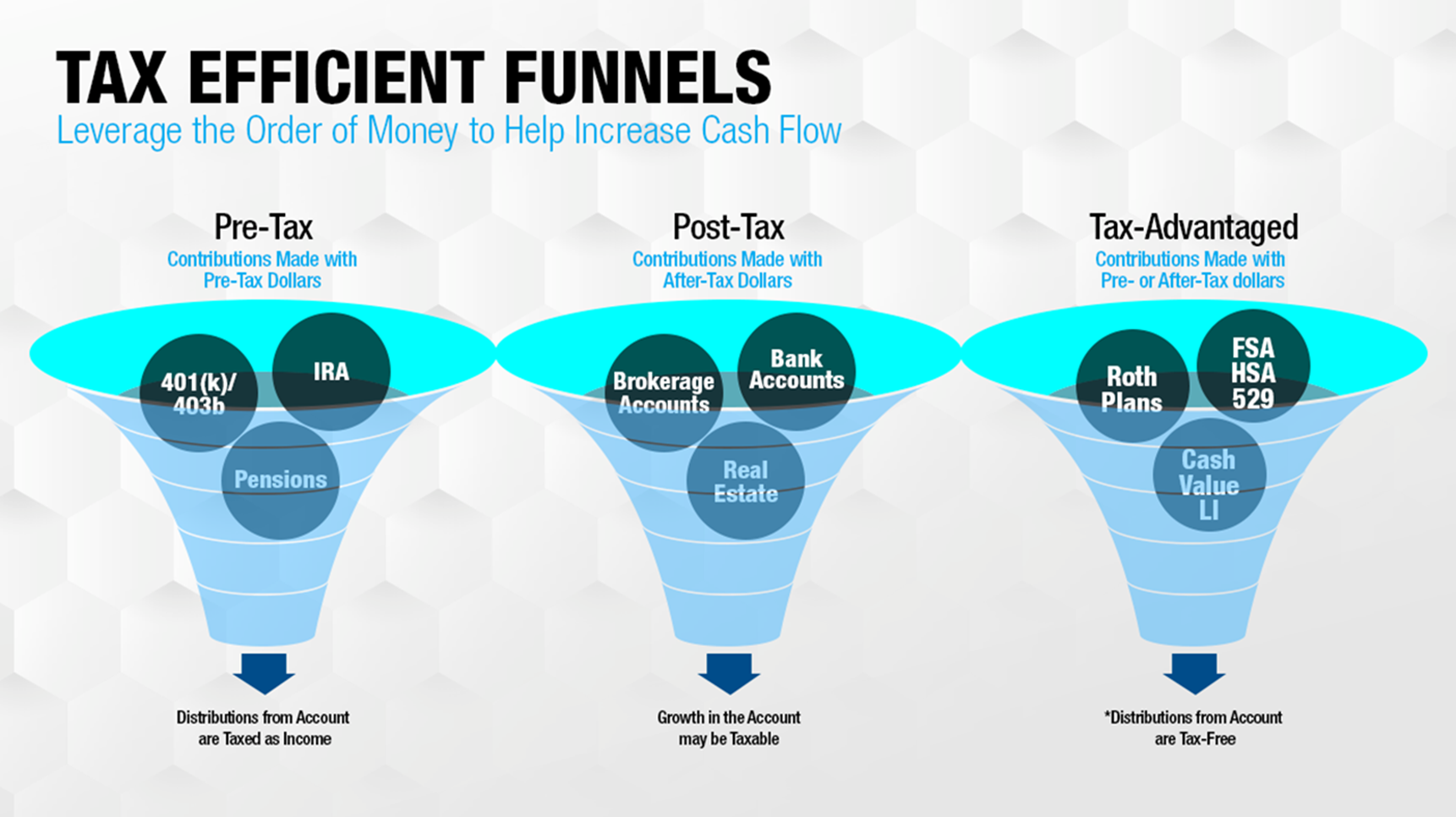

When you invest, every dollar you save falls into one of three tax funnels:

Pretax (Traditional IRA, 401(k))

After-tax (Brokerage, joint, or individual account)

Tax-free (Roth IRA, Roth 401(k), HSA)

How you manage money across these funnels determines how much you keep after taxes — not just what you earn before them.

In a taxable investment account, you face points at which gains become taxable and reduce the net return. You must manage these tax funnels proactively to keep more of your investment return. Below are key funnels, how they work, and some things to think about.

Related: 5 Reasons to Hire a Financial & Tax Planner in Retirement

1. Pretax Money

Pretax accounts give you a deduction today but come with a tax bill later.

Withdrawals are taxed as ordinary income.

Required minimum distributions (RMDs) begin at age 73.

Gains and dividends compound tax-deferred, but nothing escapes taxation in the end.

Best use: long-term growth investments where you expect to be in a lower tax bracket later. Or if you are in retirement, focusing on investments that could produce taxable income if held in an after-tax account.

2. Tax-Free Money

Tax-free accounts (Roth IRA, Roth 401(k), HSA) are the most powerful funnel for long-term compounding.

Contributions use after-tax dollars, but withdrawals in retirement are tax-free.

There are no RMDs for Roth IRAs.

HSAs, if used for medical expenses, are tax-free going in and tax-free coming out.

Best use: growth investments and assets you want to keep untouched for decades.

3. After-Tax Money

After-tax accounts are where capital gains and tax efficiency matter most. This is where many investors unknowingly trigger extra taxes.

Common tax drags:

Capital gain distributions: Mutual funds often distribute gains in December. You can owe tax even if you didn’t sell anything.

Unrealised gains turning into realised gains: Selling winners without offsetting losses increases taxable income.

Dividends: Qualified dividends are taxed at 0%, 15%, or 20%, depending on income — but reinvested dividends still count as taxable.

Things to think about:

Tax-loss harvesting: Sell investments at a loss to offset gains elsewhere. Losses can offset up to $3,000 of ordinary income, and carry forward indefinitely.

Tax-gain harvesting: In low-income years, intentionally sell appreciated assets to realise gains at 0% or 15% rates, resetting your cost basis higher.

Location management: Hold tax-inefficient investments (like active funds and bonds) inside pretax or Roth accounts, and hold tax-efficient funds (like ETFs or index funds) in after-tax accounts.

Year-End Capital Gain Distributions: The Hidden Tax Bill

Many investors don’t realise that mutual funds and active ETFs distribute capital gains every December.

These distributions are taxable, even if you reinvest them.

They can surprise you with extra taxable income — sometimes in the tens of thousands.

Check your fund company’s estimated distribution list by early November. If a large payout is expected, it may make sense to sell before the record date or hold that fund inside a tax-advantaged account next year.

Pulling It All Together

Tax-efficient investing isn’t about chasing returns — it’s about keeping more of what you earn.

Spread investments across the three tax funnels intentionally.

Pay attention to year-end distributions in after-tax accounts.

Harvest gains and losses with purpose, not emotion.

Match each investment’s tax character with the right account type.

Related: How the “Big Beautiful Bill” Reshapes Your Tax Plan

Final thoughts

The more you align your investments with the right tax funnel, the more efficient your compounding becomes. Most investors pay more tax than they need to because they ignore this simple structure. Year-end is the time to review your funnels, check for hidden distributions, and make tax-smart moves before December 31.

Related: Year-End Tax Planning Checklist

Visit my site -> finnprice.com

Education on a Weekly Basis -> Newsletter

Subscribe to the Youtube Channel for more video content -> Finn Price Youtube

About the author: Finn Price, CPFA, CEPA, is a business owner and wealth manager at Railroad Investment Group. He helps successful entrepreneurs & individuals with concentrated stock positions in their 30s, 40s and 50s build, organize, protect and transfer their wealth.

Note: this article is general guidance and education, not advice. Consult your money person or your attorney for financial, tax, and legal advice specific to your situation.

Securities and advisory services offered through LPL Financial, a registered investment Advisor, Member FINRA/SIPC.