Tax-Efficient Wealth Transfers to Children or Heirs

If you plan to leave money to your children or heirs, you need to think about taxes. Without a smart plan, a large part of your wealth could go to the government instead of your family.

Here’s what you need to know about tax-efficient wealth transfers...

First, Why Planning Matters

Passing on wealth isn't just about drafting a will. It’s about timing, method, and structure. Done right, you keep more money in your family's hands and lower future tax headaches.

Key Strategies to Use

1. Annual Gifting

You can gift up to $19,000 per person in 2025 without triggering gift taxes.

Spread gifts over the years instead of making a large lump sum transfer later.

Gifting assets likely to appreciate moves future growth out of your taxable estate.

2. Lifetime Exemption Use

The lifetime gift and estate tax exemption is $13.99 million in 2025, but is scheduled to be cut in half after 12/31/2025. This could be extended if TCJA is extended, but that has not occurred yet.

Now is the time to shift assets if you want to use the larger exemption before it shrinks.

Below is a table of the historical estate tax exemption amounts:

3. Irrevocable Trusts

Move assets into a trust to remove them from your estate.

Trusts allow you to control how and when heirs receive money, protect against creditors, and sometimes lower income taxes.

4. Family Limited Partnerships (FLPs)

Transfer ownership interests in businesses or real estate at a discount.

Keep control while moving value to heirs tax-efficiently.

5. Step-Up in Basis Planning

Assets like stocks and real estate get a “step-up” in basis at death.

Sometimes, it’s better to hold appreciated assets until death rather than gift them early.

Careful balance is key between lifetime gifting and holding for a step-up.

6. Roth IRA Conversions

Roth accounts pass to heirs income tax-free.

Converting traditional retirement accounts to Roth during your lifetime could save your heirs big future tax bills.

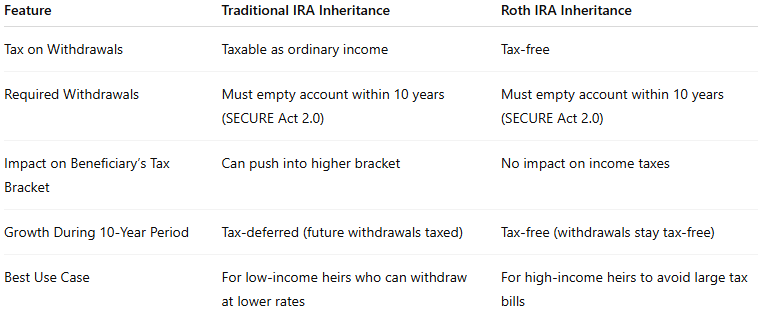

Why Traditional IRAs Create Tax Problems for Heirs

Even if your estate is below the exemption amount, traditional IRAs can create a hidden tax burden. Here’s why:

Under the SECURE Act 2.0, non-spouse beneficiaries must fully withdraw inherited IRA funds within 10 years.

Those withdrawals are taxed as ordinary income to the heirs.

If your heirs are high earners, it could push them into higher tax brackets.

There’s no stretch IRA anymore to spread the tax hit over their lifetime.

This means a $1 million traditional IRA could potentially lose $300,000 to $400,000 or more to taxes, even if no estate tax is due.

Related: Guide to the 3 Tax Funnels: Where Should Your Next Investment Go?

Why Roth IRAs Are So Valuable for Heirs

Roth IRAs are powerful tools for wealth transfer:

Tax-Free Withdrawals: Beneficiaries can take money out tax-free.

Still Subject to 10-Year Rule: They must empty the account within 10 years, but without a tax bill at each withdrawal.

Flexible Growth: Funds inside the Roth keep growing tax-free during the 10 years if withdrawals are delayed.

In short, Roth accounts remove the income tax risk from inherited retirement assets. They can preserve hundreds of thousands of dollars for your family compared to traditional IRAs.

Here is a table to compare the two accounts:

Mistakes to Avoid

Waiting too long: Rushing planning after a major health event or death limits your options.

Ignoring income taxes: Focus on estate taxes and the income taxes heirs will pay.

Overcomplicating it: Complex structures only make sense if the tax savings outweigh the legal and administrative costs.

The Bottom Line

A good wealth transfer plan is simple, tax-smart, and flexible. Start planning early while tax laws are still favorable. Your heirs will thank you.

Related: Maximize Wealth Transfer: 2025 Gifting Rules and Tax-Saving Strategies

Visit my site -> finnprice.com

Business Owner Education on a Weekly Basis -> Newsletter

Subscribe to the Youtube Channel for more video content -> Finn Price Youtube

About the author: Finn Price, CPFA, CEPA, is a business owner and wealth manager at Railroad Investment Group. He helps successful entrepreneurs & individuals with concentrated stock positions in their 30s, 40s and 50s build, organize, protect and transfer their wealth.

Note: this article is general guidance and education, not advice. Consult your money person or your attorney for financial, tax, and legal advice specific to your situation.

Securities and advisory services offered through LPL Financial, a registered investment Advisor, Member FINRA/SIPC.